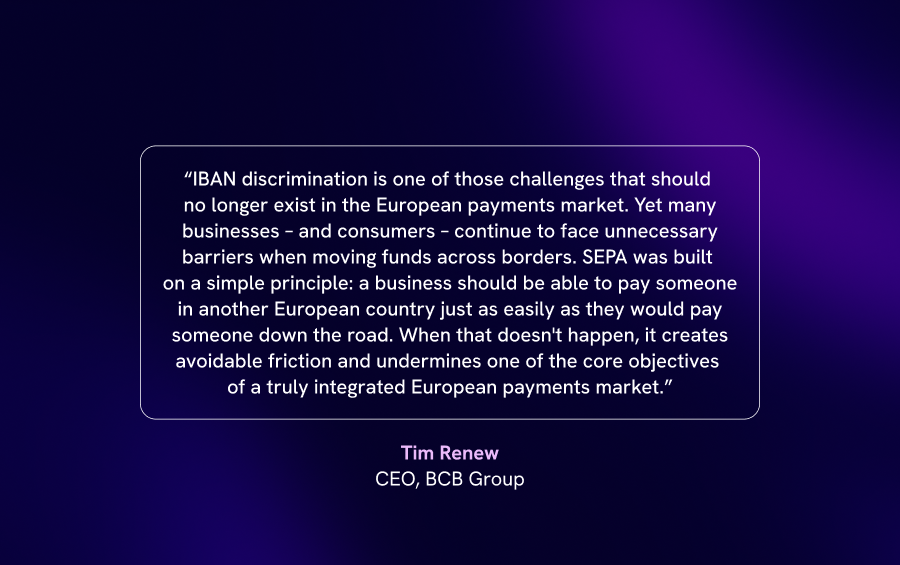

What is IBAN discrimination and why does it still matter in Europe?

The Single Euro Payments Area (SEPA) was designed to make cross-border euro payments as simple and seamless as domestic transactions. That means a business should be able to send and receive payments from any SEPA account regardless of where that account is located.

Unfortunately, as we will explain in this article, this is not always the case.

How does IBAN discrimination work?

This is when a bank, company or service provider refuses to accept a SEPA payment to or from an account because it is based in a different country. Although IBAN discrimination is prohibited under EU law, it remains a relatively common problem across Europe.

In France, for example, the General Directorate for Competition, Consumption and Fraud Control (DGCCRF) and the National Committee for Cashless Payments (CNPS) can issue fines to organisations that discriminate against non-French bank accounts, with penalties of up to €75,000 for individuals and €375,000 for legal entities.

The legal position is clear – so why is IBAN discrimination still so common?

For businesses operating across multiple European markets, IBAN discrimination is still a persistent operational challenge that can affect everything from the customer experience to treasury efficiency.

One of the underlying factors is that payment ecosystems are not just influenced by regulation – because financial institutions also assess the risks associated with counterparties, partners and customers.

These assessments are influenced by compliance standards, operational controls, regulatory supervision and the need to minimise financial and reputational risk.

In practice, regulatory permission is not the determining factor – risk perception is.

The importance of market reputation

Different regulatory regimes across Europe are often perceived differently by banks, counterparties and institutional customers. Some jurisdictions are widely regarded as having more rigorous supervisory standards and robust compliance expectations. Others may be viewed differently based on the maturity of their regulatory infrastructure, historical market experience and the types of institutions that have traditionally operated in their locations.

As a result, these views are often shaped as much by market perception as by the underlying regulation itself.

Banks and counterparties frequently make decisions that are not just based on regulatory requirements, but on how comfortable they feel with the regulatory environment that a particular institution operates in.

This can help to explain why IBAN discrimination has persisted despite the fact that not only is it prohibited under EU law, it also undermines the purpose of SEPA, which is to enable seamless cross-border euro payments so they are treated in the same way as domestic payments.

Understanding the scale of IBAN discrimination

The Accept My IBAN initiative, which is supported by organisations including Starling Bank, Wise and Revolut, is calling for stronger enforcement and more consistent action from European authorities.

Consumers are also affected

Data collected by the The Accept My IBAN initiative suggests that hundreds of consumers each month continue to encounter difficulties paying for services because their IBAN originates from another European country.

These rejected payments, delayed settlements and additional compliance checks can all create avoidable operational friction that should not exist within a single payments area.

While stronger enforcement will be vital for putting an end to this discrimination, the industry also needs to collaborate more closely to raise awareness of this problem and reduce barriers across the European payments ecosystem.

Why can IBAN jurisdiction affect payment acceptance, even within SEPA?

IBAN discrimination is still a significant challenge for pan-European operators, fintechs, payment companies as well as digital asset firms that rely on efficient cross-border payment flows.

Under EU law, although all SEPA IBANs should be treated equally, the reality is that some IBAN jurisdictions may still be treated differently by counterparties, banks or payment recipients.

This may not be a reflection of the quality of the business itself, but rather of broader perceptions around regulatory oversight, compliance standards and market confidence in the jurisdiction in which the business operates.

As a result, these businesses may encounter more complex onboarding requirements, extensive reviews or increased payment friction simply because of how their particular jurisdiction is perceived by the wider market.

How can IBAN discrimination create practical friction for businesses?

1. Rejected payments

The most obvious consequence of IBAN discrimination is the rejection of legitimate payment instructions.

This prevents customers from accessing essential services, while businesses can experience payment disruption, more operational complexity and reduced customer satisfaction.

What should be a simple, predictable payment can quickly escalate into a complicated support issue that needs to be manually investigated – and the inevitable outcome is delayed settlement.

2. Delayed settlements

Any settlement delays create avoidable operational friction.

Even minor friction can materially reduce cash flow visibility and slow onboarding.

This can have serious consequences for digital asset firms, fintechs and payment companies operating across multiple markets and relying on the uninterrupted movement of funds.

Every rejected or delayed payment generates additional work somewhere within the organisation.

- Operations teams may need to investigate the issue.

- Customer-facing teams may need to respond to complex enquiries.

- Finance teams may need to reconcile transactions manually.

As payment volumes increase, these additional costs can compound – rapidly diverting resources away from other potentially high-value activities.

3. Treasury uncertainty

Reliable treasury management depends on predictability.

Without predictable payment flows, treasury teams will find it harder to maintain full visibility over their incoming and outgoing funds. This means they are forced to rely on larger liquidity buffers, spend more time producing cash flow forecasts or introduce additional operational controls to manage uncertainty.

These challenges can ultimately affect efficiency, scalability and overall business performance.

Looking beyond transaction costs

While it is easy to focus solely on transaction costs when assessing modern payments infrastructure, there is arguably a much larger cost associated with payment friction.

A delayed payment can require significant manual intervention from operations teams. They may need to investigate the issue, handle customer enquiries and spend additional time reconciling transactions.

This can create liquidity management challenges and make treasury forecasting more difficult. These hidden costs are unlikely to be reflected in simple headline pricing comparisons, but they can have a significant impact on operational efficiency.

As businesses scale, reliability and predictability can become much more valuable than any marginal difference in headline transaction pricing. Businesses are increasingly dependent on the ability to move funds consistently and predictably in order to create operational efficiencies that support long-term growth.

Why licences in Tier-1 jurisdictions are still perceived differently

Regulatory regimes across Europe are not viewed identically by banks, customers, regulators and counterparties.

Some jurisdictions have developed reputations for particularly rigorous supervision, demanding compliance requirements and close regulatory oversight.

This does not mean that institutions licensed elsewhere are not regulated. Rather, it reflects how the market views different regulatory environments.

These perceptions can influence everything from banking relationships and onboarding decisions to how payment flows are treated throughout the wider financial ecosystem.

Institutions operating within regulatory regimes that are widely regarded as demanding and credible often benefit from stronger market confidence. Banks may be more comfortable establishing relationships, counterparties may require fewer additional reviews and customers may have greater confidence in the institution’s operating model.

This greater confidence across the payment chain can contribute to more predictable payment flows, fewer operational interruptions and a smoother experience when moving funds across borders.

Why should a customer care about a provider’s licensing position?

Customers do not choose a payments partner just because it holds a licence in a particular jurisdiction.

What matters much more to them is having the assurance that their payments will be processed reliably, counterparties will engage constructively, and the partner’s infrastructure will continue to support their long-term growth.

Therefore, building and maintaining strong regulatory credibility becomes commercially relevant when it has a material impact on customer outcomes.

BCB’s licensing footprint reflects a regulatory-first approach and a commitment to operating within jurisdictions that are widely regarded as having demanding supervisory standards. In practice, this can improve market confidence, support robust compliance processes and create a valuable gateway to high-quality banking relationships.

How does BCB translate this into customer value?

1. Certainty of transaction

For customers, the most important outcome is certainty.

Businesses need confidence that payments will be processed efficiently and consistently, without unnecessary friction or avoidable delays.

A strong regulatory foundation helps support that certainty by creating confidence among banking partners, counterparties and customers throughout the payment chain. Combined with infrastructure such as BLINC, BCB’s institutional settlement network, this can enable predictable payment flows for customers that need flexible liquidity and faster settlements across multiple markets.

2. Robust compliance

BCB’s regulatory footprint reflects its commitment to operating within mature regulatory frameworks – as this ensures customers benefit from a higher-grade compliance environment that promotes long-term stability and resilience.

3. Access to high-quality banking relationships

Strong regulatory standing can also support access to high-quality banking relationships.

These relationships form an important part of the wider payments ecosystem and contribute to the reliability, resilience and predictability that institutional customers increasingly require.

While these advantages may not always be visible in headline pricing comparisons, they can have a significant impact on operational performance. Fewer failed transactions, reduced payment friction and less operational disruption can ultimately create value that extends well beyond transaction costs alone.

What should you do if you have experienced IBAN discrimination?

If you believe you have been the victim of IBAN discrimination, the European Commission recommends submitting a complaint to the relevant national competent authority in the country where the discrimination occurred.

Although IBAN discrimination remains illegal under EU law, continued reporting and enforcement will be important to improving compliance across the European payments ecosystem.

For businesses, payment reliability is not only about technology. It is also about regulatory trust, banking relationships and market perception.

Organisations evaluating payments infrastructure should therefore look beyond headline pricing and consider the wider operational impact of their provider’s regulatory standing and banking network. While a lower-cost option may appear attractive initially, the hidden costs associated with failed payments, settlement delays, additional requirements and treasury uncertainty can quickly outweigh any upfront savings.

BCB’s Tier-1 licensing footprint is much more than a compliance credential. It reflects the firm’s ongoing commitment to operating within demanding regulatory environments that support market confidence, higher-quality banking relationships and greater certainty of transaction.

For customers, the outcome is fewer failed transactions, reduced payment friction, greater operational resilience and a payments infrastructure designed to deliver reliability when it matters most.

Contact us to find out more about IBAN discrimination and how BCB Group can help your business today.

Related Insights

What are agentic payments and why do they matter?

READ

BCB Group is shortlisted for four awards at the Women in Tech Employer Awards 2026

READUnderstanding modern remittance infrastructure

READ

How modern settlement infrastructure helped BLINC gain dominance

READ

BCB Group on the importance of remittances within the financial ecosystem

READ

The Fintech Times Coverage of BCB Groups award win

READWhy Remittance Firms Are Embracing BLINC

READ